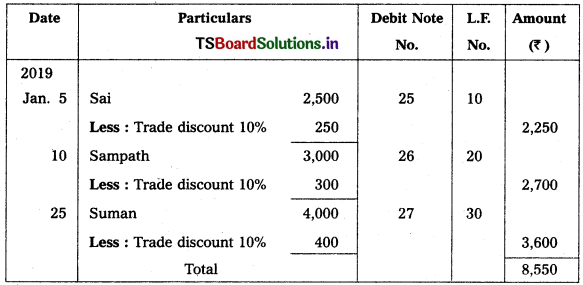

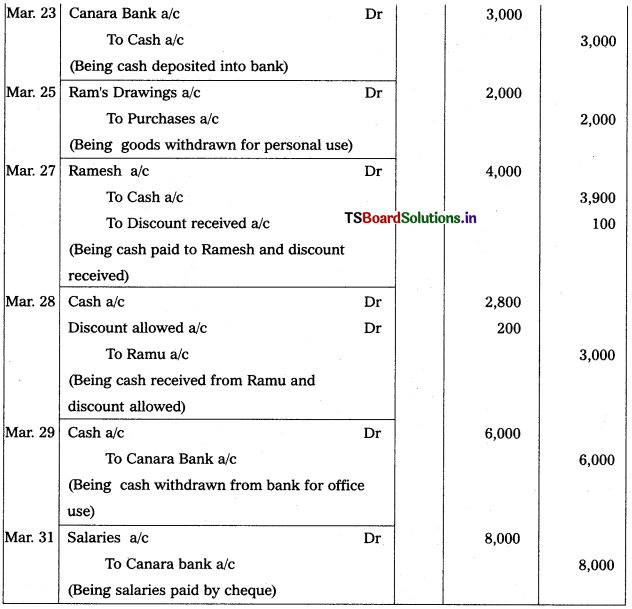

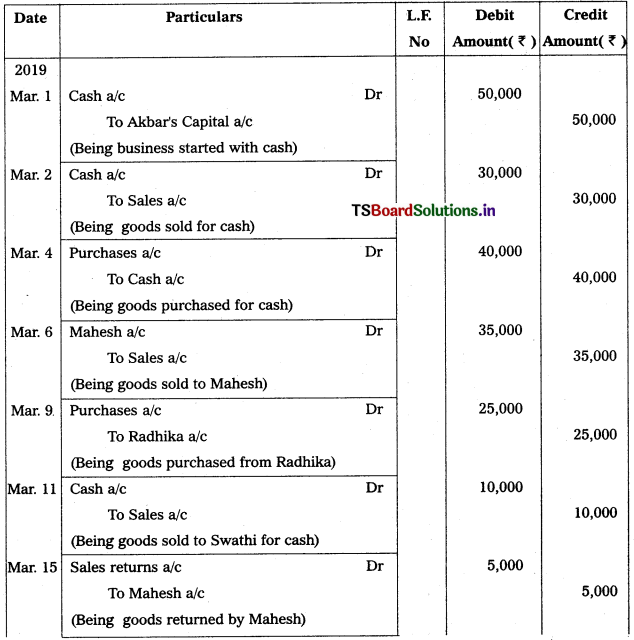

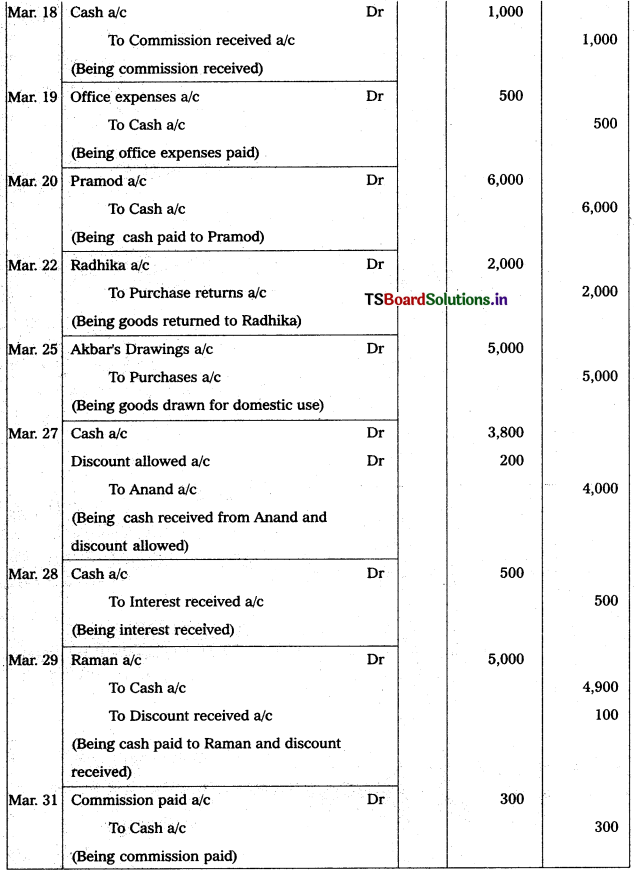

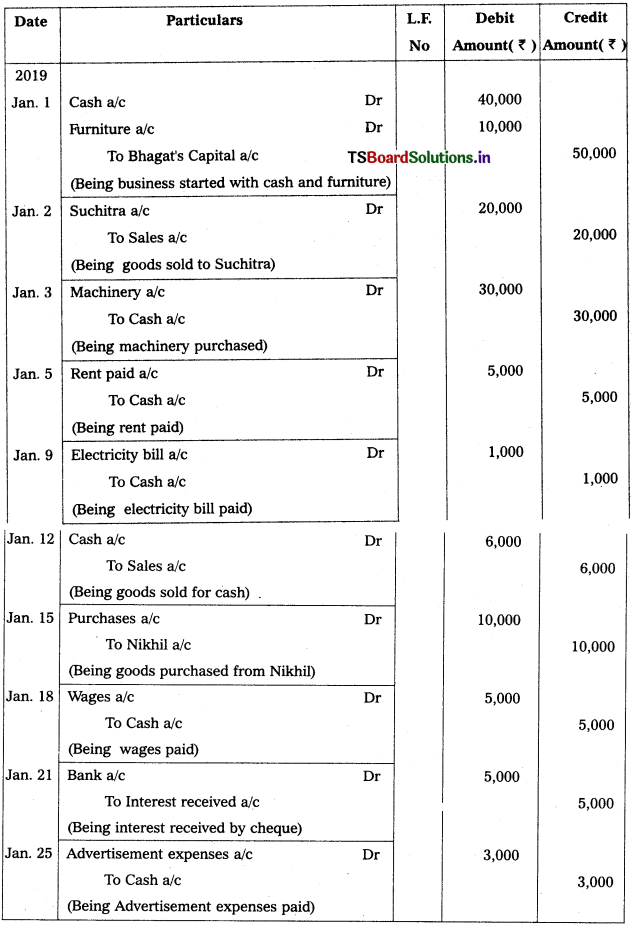

Telangana TSBIE TS Inter 1st Year Hindi Study Material Grammar वर्तनी, शब्द विचार, उपसर्ग, प्रत्यय Questions and Answers.

TS Inter 1st Year Hindi Grammar वर्तनी, शब्द विचार, उपसर्ग, प्रत्यय

హిందీ మన దేశపు జాతీయ భాష కాక అధికార భాష కూడా. ఇప్పుడు ఈ భాష మనదేశంలోనే కాక ప్రపంచంలో సుమారు 170 విశ్యవిద్యాలయాల్లో భోదించబడుతుంది పరిపాలన, బ్యాకింగు, వాణిజ్య వ్యాపారాలు, పత్రికారంగం, ప్రసార మాధ్యమాలు మొదలైన వాటన్నింటిలో హిందీ వ్యాప్తి క్రమేపి పెరుగుతూ వస్తోంది. ఇలా ప్రాచుర్యం పెంచుకుంటున్న హిందీ భాష యొక్క శుద్ద రూపాన్ని (correct form) నేర్చుకోవటం. మాట్లాడటం, వ్రాయడం చాలా అవసరం. భాష యొక్క శుద్ధ రూపాన్ని मानक भाषा [standard Language] అంటారు. విద్య, పరిపాలన తదితర రంగాల్లో हिन्दी యొక్క मानक रूप మాత్రమే ఉపయోగపడుతుంది.

हिन्दी भाषा యొక్క मानक रूप ని నేర్చుకోవటం కోసం క్రమం తప్పకుండా చదవటం, వ్రాయటం చాలా అవసరం. పదాల ఉచ్చారణ – వ్రాత (लेखन) పట్ల దృష్టి కేంద్రీకరించాలి. दोष (Mistakes) లేకుండా ఉండేందుకు ఎల్లప్పుడూ జాగరూకులై ఉండాలి. वर्तनी दोष [Spelling] విషయంలో నిర్లక్ష్యం ఎంత మాత్రం తగదు. క్రమం తప్పని అభ్యాసంతో షెగే ని నివారించవచ్చు.

हिन्दी యొక్క ప్రస్తుత రూపం खड़ीबोली, దీని లిపిని देवनागरी అంటారు. लिपि యొక్క సరియైన రూపాన్ని బాగా అర్థం చేసుకుంటే वर्तनी दोष రాకుండా జాగ్రత్త పడవచ్చు. ఉచ్చారణే వ్రాతకు ఆధారం కనుక స్పష్టమైన ఉచ్చారణ అభ్యసించటం చాలా అవసరం.

अ) वर्णमाला :

स्वर : अ आ इ ई उ ऊ ऋ

ए ऐ ओ औ अं अः

व्यंजन : क ख ग घ ङ

च छ ज झ ञ

ट ठ ड ढ ण

त थ द ध न

प फ ब भ म

य र ल व

श ष स ह

क्ष त्र ज्ञ

वर्ण (परिभाषा) : ‘लिखित भाषा की उस छोटी से छोटी मूल ध्वनि को वर्ण कहते हैं, जिसके टुकड़े नही किए जा सकते’ । मूल रूप में वर्ण वे चिह्न हाते हैं, जो हमारे मुख से निकली हुई ध्वनियों के लिखित रूप होते हैं ।

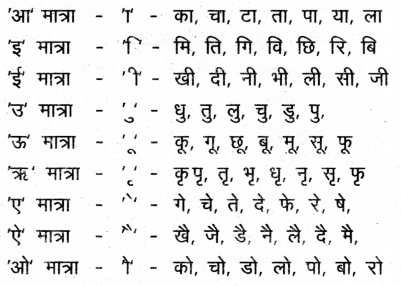

आ) मात्राएँ :

इ) हस्व और दिर्घ : ఉచ్చారణ వ్రాతల్లో ‘हस्व’, ‘दीर्घ’, యొక్క తేడాను గమనించాలి.

a) जब उच्चरण अल्प होता है, तब उस ध्वनि को ह्रस्व कहा जाता है ।

b) जब उच्चरण दीर्घ होता है, तब उस ध्वनी का दीर्घ कहा जाता है ।

(इ, उ मात्राएँ)

नियम, विजय, सितार, किसान

मिठाई, विपुल, गिलास, बिल्ली

बुराई, पुस्तक, लुहार, बुढ़ापा

सुनार, कुम्हार, गुड, भुलाना

(ई, ऊ मात्राएँ)

कीमत, गीत, खीर, पीर

वीर, क्षीर, भाई, नीरज

पूर्व, भूत, मूर्ख, दूध

झूला, दूसरा, पेटू, चूहा

ई) अल्प प्राण और महा प्राण : హల్లులు (व्यंजन) లోని ప్రతి వర్గపు మొదటి అక్షరాన్ని ‘अल्प-प्राण’ అని, రెండవ అక్షరాన్ని ‘महा-प्राण’ అని వ్యవహరిస్తారు. ఒకటి ఉచ్చరించ / వ్రాయవలసిన చోట మరొకటి ఉపయోగించటం తప్పు.

उदा : अल्प प्राण – क, च, ट, त, प

महा-प्राण – ख, छ, ठ, थ, फ

अशुद्ध (✗) – शुद्ध (✓)

बोजन – भोजन

आँक – आँख

तोडा – थोड़ा

रोठी – रोटी

चाया – छाया

पूल – फूल

चतरी – छतरी

उ) अनुनासिकता और अनुस्वार : హిందీలో అనునాసిక శబ్దాల సంఖ్య చాలా హెచ్చు చాలా శబ్దాలు अनुस्वार జోడించడం ద్వారా बहुवचन గా మారతాయి. अनुस्वार चंद्र बिन्दा (ँ) లేక (बिन्दी) (.) చేర్చటం ద్వారా వ్యక్తమౌతాయి. వీటిని ఉచ్చారణ వ్రాతల్లో విధిగా పాటించాలి.

उदाहरण :

गाय – गायें

आँख – आँखें

काँटा – काँटे

बहन – बहनें

माता – माताएँ

बहूएँ – बहू

रानी – रानियाँ

दवा – दवाएँ

चिडिया – चिड़ियाँ

बुढिया – बुढ़ियाँ

परीक्षा – परीक्षाएँ

लड़की – लड़कियाँ

मछलियाँ – मछली

महिला – महिलाएँ

स्त्री – स्त्रीयाँ

ऊ) पर भाषा शब्द : హిందీలో చాలా శబ్దాల अरबी, फारसी మరియు భాషల నుండి వచ్చినవి. తారసపడతాయి. వాటిని సరిగా ఉచ్చరించటం కోసం అక్షరం క్రింద ఉంచబడుతుంది.

उदाहरण : अंदाज, कागज, काजल, कमीज, कफन, फायदा, जागीर, एतराज़, इल्जाम, जरा, आजाद, पाजटिव, जीरों, डज़न, जेबरा, आदि ।

ॠ) ‘ऋ’ मात्रा का सही प्रयोग : ‘ऋ’ मात्रा (c) వ్రాయవలసిన చోట (‘र’) मात्रा दुई తో వ్రాయటం తప్పు.

उदाहरण :

अशुद्ध (✗) – शुद्ध (✓)

प्रुथ्वी – पृथ्वी

क्रुष्ण – कृष्ण

स्रुटि – सृष्टि

क्रुपा – कृपा

ए) ‘र’ का संयुक्ताक्षर : హిందీలో (‘र’) ధ్వని మూడు రకాలుగా సంయుక్తాక్షరంగా వ్రాయబడుతుంది.

प्र – क्रम, ग्रंथ, व्रत, प्रचार, भ्रमर, द्रविड, आदि ।

र्प – धर्म, कर्म, मर्म, गन्धर्व, आर्य, पर्व आदि ।

ट्र – राष्ट्र, दंष्ट्रा उष्ट्र, पौण्ड्रवर्धन, आदि ।

ऐ) ‘घ’ और ‘ध्य’ : ‘द्य’ వ్రాయవలసిన చోట ‘ध्य’ వ్రాయటం, ఉచ్చరించుట తప్పుగా పరిగణింపబడుతుంది. ‘द’ ని ఉచ్చరించవలసిన చోట ‘ध्य’ ప్రయోగించాలి.

उदाहरण :

अशुद्ध (✗) – शुद्ध (✓)

खद्य – खाद्य

विद्या – विद्या

मद्यपान – मद्यपान

विध्यार्थी – विद्यार्थी

विध्यलय – विद्यालय

पध्य – पद्य

ओ) ‘ध्य’ केल००’ ‘द्य’ వ్రాయటం ఉచ్చరించుటం తప్ప .

उदाहरण :

अशुद्ध (✗) – शुद्ध (✓)

अद्याय – अध्याय

उपाधाय – उपाध्याय

अद्यापक – अध्यापक

औ) ‘ए’ और ‘ये’ का प्रयोग : క్రియారూపంలో ‘ए’ మరియు ‘ये’ ప్రయోగించటం విషయంలో జాగ్రత్త వహించాలి. క్రియ పూర్ణకాలికమైతే ये, క్రియ, विधि స్వరూపమైతే ఉపయోగించాలి.

उदाहरण :

अशुद्ध (✗) – शुद्ध (✓)

गाया – गाये

दिया – दिये

सोया – साये

आया – आये

रोया – रोये

दीजिये – दीजिए

बैठिये – बैठिए

लाइये – लाइए

खाइये – खाइए

शुद्ध वर्तनी केलिए नियम

- भाषा में उच्चारण की स्पष्टता लानी होगी, जब उच्चारण ठीक हो, तो वर्तनी भी ठीक होगा । क्योंकि देवनागरी लिपि ऐसी वैज्ञानिक लिपि है कि जो पढा जाता है, वही लिखा जाता है ।

- निरंतर पढने – लिखने के अभ्यास से वर्तनी दोषों पर रोक लगायी जा सकती है ।

- स्वर – व्यंजन, हलंत – लिंग, वचन, प्रत्यय, संधि, समास आदि के प्रयोग में निरंतर अभ्याय की जरूरत है ।

హిందీలో వ్రాతను మెరుగుపరచుకోవాలంటే ముందు ఉచ్చారణ స్పష్టంగా ఉండేలా చూసుకోవాలి. ఉచ్చారణ సరిగ్గా ఉంటేనే అక్షర దోషాలు రాకుండా ఉంటాయి. దేవనాగరి లిపిలో ఉచ్చారణ ఎలా ఉంటుందో వ్రాత కూడా అలాగే ఉంటుంది. కాబట్టి ముందుగా ఉచ్చారణ సరి చేసుకుంటే చాలా వరకు వ్రాతలోని అక్షర దోషాలను నివారించవచ్చు. దీనికి ఒకటే మార్గం. నిరంతరం చదవడం, వ్రాయడం చదువుతూ ఉంటే మన కళ్ళతో అక్షరాలకు ఒక రిలేషన్ లాంటిది ఏర్పడాలి. దానినే ‘చక్షురక్షర సంయోగం’ అంటారు. ఇది ఒక్కసారి కుదిరిందంటే ఇక వ్రాసేటప్పుడు అక్షర దోషాలు రావు.

हिन्दी में वर्तनी दोषों के असंख्य उदाहरण बन सकते हैं जिनका उल्लेख करना यहाँ संभव नही है । अतः उदाहरण के लिए जिन शब्दों के साथ अधिक वर्तनी – दोष पाये गये हैं उनका यहाँ प्रस्तुत किया जा रहा है ।

హిందీ వ్రాసేటప్పుడు అసంఖ్యాకమైన అక్షర దోషాలు విద్యార్థులలో కనబడతాయి. అయితే వాటన్నింటినీ ఇక్కడ ప్రస్తావించడం కష్టం. కాబట్టి ఉదాహరణ కోసం కొన్ని అక్షర దోషాలను ఇక్కడ ఇవ్వడం జరుగుతున్నది.

अशुद्ध रूप – शुद्ध रूप

टंडा – ठंडा

अहार – आहार

आदमि – आदमी

आरामान – आसमान

अन्यधा – अन्यथा

अत्याधिक – अत्यधिक

आँक – आँख

ईक – ईख

इमलि – इमली

उन्नति – उन्नति

उपनयास – उपन्यास

उध्योग – उद्योग

ऊचा – ऊँचा

चांद – चाँद

घंठा – घंटा

काना – खाना

बादा – बांधा

धोका – धोखा

पौदा – पौधा

ग्यान – ज्ञान

दीर्घ – दीर्घ

भूक – भूख

बिक्षुक – भिक्षुक

पंढित – पंडित

पुरानि – पुरानी

वस्तू – वस्तु

आँसु – आँसू

निष्टा – निष्टठा

पूजारी – पुजारी

हमेसा – हमेशा

लीखिए – लिखिए

दीजीए – दीजिए

प्रतिक्षा – प्रतीक्षा

उत्तीण – उत्तीर्ण

प्रवेस – प्रवेश

परकाश – प्रकाश

यात्र – छाञ

राष्ट्र – राष्ट्र

शरन – शरण

बारत – भारत

अभ्यास

(✗) – (✓)

पुरसकार – पुरस्कार

प्रर्दसन – प्रदर्शन

सममेलन – सम्मेलन

मचली – मछली

बोजन – भोजन

कृष्ण – कृष्ण

विध्यार्थी – विद्यार्थी

स्मरन – स्मरण

पूस्तक – पुस्तक

हीन्दी – हिन्दी

कताब – किताब

गूण – गुण

धरमात्मा – धर्मात्मा

गोर – घोर

भादा – बाधा

कारन – कारण

प्रान – प्राण

कन – कण

उदहरण – उदाहरण

इस्पष्ट – स्पष्ट

सीक – सीख

पच्चिस – पच्चीस

कर्तब्य – कर्तव्य

शब्द विचार

जिसने शब्दों के भेद ( उनके प्रयोग) रूपांतर और व्युत्पति का निरूहण किया जाता है, उसे शब्द साधान (या) शब्द विचार कहते है ।

ధ్వనుల కలయికతో ఏర్పడే అర్థపూరిత అక్షర సమూహాన్ని ‘शब्द’ అంటారు. ప్రతి ‘शब्द’ కి దాని అర్థం ఉంటుంది. ఏ ‘शब्द’ ల అర్థం స్పష్టంగా వ్యక్తమౌతుందో వాటిని ‘सार्थक शब्द’ అంటారు. ఏ భాషలోనైతే ఒక शब्द కి అర్థం ఉండదో దానిని ‘निरर्थक शब्द’ గా పరిగణిస్తారు. హిందీ భాషలో कल’ सार्थक शब्द’ అని, దీనికి సందర్భాన్ని బట్టి ‘నిన్న’, ‘రేపు’, ‘యంత్రము’ అనే అర్థాలున్నాయి. కాని लक ఈ భాషలో नरर्थक शब्द, అలాగే नरर्थक शब्द’, ‘जल’, सार्थक, ‘लज’, निरर्थक అని చెప్పవచ్చును.

परिभाषा : ఒకటి లేక అంతకంటే ఎక్కువ అక్షరాలు అర్థపూరితమైన కలయికతో ఏర్పడే దాన్ని ‘शब्द’ అంటారు. ‘जा’, ‘खा’, ‘गा’ ‘आ’ మొదలైనవి. ఏకాక్షర శబ్దాలు ‘चिड़िया’, ‘पहाड़’, ‘आसमान’ మొదలైనవి ఏకాధిక అక్షరాలతో ఏర్పడిన శబ్దాలు.

शब्दों के प्रकाश : కొన్ని ‘शब्द’ ఒకే అర్థానిచ్చేవిగా ఉంటాయి. వాటిని అని అంటారు. ఉదా : स्वागत, यश, कृपा, पुस्तक వీటికి ఏ సందర్భంలోనైనా ఒకే అర్థం గోచరిస్తుంది. కొన్ని ‘शब्द’ బహు అర్థాలు ఇచ్చేవిగా ‘अनेकार्थी शब्द’ అంటారు. వేర్వేరు సందర్భాలలో ఒక్క. ‘शब्द’ కే వేర్వేరు అర్ధాలు ఉంటాయి.

उदा : अर्थ = कारण, मतलब, लिए, धन

पानी = जल, सम्मान, प्रतिष्ठा, चमक

कर = क्रिया, हाथ, किरण, लगना, सूँड ।

కొన్ని शब्द ‘समानार्थक शब्द’ గా ఉంటాయి.

उदा : बंधु और मित्र

दक्ष, कुशल और निपुण

शोक और दुख

कष्ट और पीड़ा

आज्ञा और आदेश

शब्द కు ‘विपरीतार्थक शब्द’ కూడా ఉంటాయి.

उदा : मान – अपमान

अग्रज – अनुज

उत्तम – अधम

अल्पायु – दीर्घायु

उदय – अस्त

उच्च – निम्न

आय – व्यय

आजादी – गुलामी

शब्दों का एक प्रकार : ధ్వని సంబంధమైన అనుకరణనం బట్టి కూడా ఉంటుంది. పశుపక్ష్యాదుల అరుపులు, ధ్వనులు ప్రతి భాషలో తనశైలిలో అనుకరించబడతాయి. హిందీలో ఇటువంటి ధ్వనుల అనుకరణ క్రింది విధంగా ఉంటుంది.

चिड़ियाँ खनकती हैं ।

घड़ी टिक-टिक चलती है ।

शेर दहाड़ता है ।

बिल्ली म्याऊँ म्याऊँ करती है ।

कुत्ता भौकता है ।

कौआ कॉव-कॉव करता है ।

गधा रेंकता है ।

मुर्गा कूंकडूं कूँ करता है ।

दिल धक धक करता हैं ।

बादल गरजते हैं ।

बिजली कड़कती है ।

ఇతర భాషలవలె हिन्दी లో కూడా मुहावरे और कहावतें ఉంటాయి. వీటికి సామాన్య అర్థంకాక విశిష్టమైన అర్థం వ్యక్తమౌతుంది.

ఉదా : अँगूठा दिखाना जरूरत होने पर धोखा देना

आम के आम गुठलियों के दाम = बहुत फायदा होना

शब्द स्त्रोत భాష దృష్ట్యా హిందీ – సంస్కృతం యొక్క అనేక ‘मूल शब्द’ యధాతథంగా ఒకేలా ఉంటాయి. కాని అనేక సంస్కృత భాషా శబ్దాలు పాళి, ప్రాకృత, అపభ్రంశ భాషల్లోకి వెళ్ళి మార్పుచెంది హిందీలోకి ప్రవేశించాయి. మరికొన్ని శబ్దాలు హిందీ భాషా ప్రాంతాల్లోని వివిధ ఉపభాషల నుండి हिन्दी లోనికి వచ్చాయి. ఇంకొన్ని విదేశి భాషల శబ్దాల్ని हिन्दी भाषा గ్రహించింది. ఈ రకంగా हिन्दी లో నాలుగు రకాలైన शब्द ఉంటాయి. तत्सम तद्भव, देशज तथा विदेशी ।

1. तत्सम : హిందీ భాషలో చెలామణిలో ఉన్ संस्कृत मूल शब्द ను ‘तत्सम शब्द’ అంటారు अग्नि, पुष्प, चतुर्थ, मयूर, क्षीर మొదలైన సంస్కృత శబ్దాలు హిందీలో యధాతదంగా ప్రయోగింపబడతాయి. ఇటువంటి శబ్దాల సంఖ్య హిందీలో వేలాదిగా ఉంటుంది.

2. तद्भव : సంస్కృత భాష నుండి ప్రాకృతంలోనికి వెళ్ళి మార్పుచెంది ‘హిందీ భాషలోనికి వచ్చిన శబ్దాల్ని ‘तद्रभव शब्द’ అంటారు.

संस्कृत – हिन्दी

मया = मैं

उष्ट्र = ऊँट

आम = आम

मयूर = मोर

मध्य = में

दन्त = दांत

तिक्त = तीता

शत = सौ

चंचु = चोंच

पुष्प = फूल

घोटक = घोड़ा

चतुर्थ = चौथा

क्षीर = खीर

त्वरित = तुरंत

वन्स = बच्चा

भक्त = भात

नव = ना

सूचि = सुई

3. देशज : ఏ శబ్దాలైతే हिन्दी भाषा ప్రాంతాల్లో వ్యాప్తిలో ఉన్న ఉప భాషల నుండి हिन्दी లోకి వచ్చాయో, వాటిని ‘देशज शब्द ‘ అంటారు.

उदा : कटरा, पाडा, तेन्दुआ, खिडकी, कटोरा, चिड़िया, ठुमरी, जूता, खिचडी, लोटा, डोल, डाब, डोंगी, पगडी, कलाई, ठेठ, डिबिया మొదలైనవి ఈ కోవకు చెందిన శబ్దాలే.

4. विदेशी : ఏ శబ్దాలైతే విదేశీ భాషల నుండి हिन्दी లోనికి వచ్చాయో, . వాటిని ‘विदेशी शब्द’ అంటారు. अरबी, फारसी, तुर्की, पुर्तगाली, మొదలైన భాషల్లోని వేలాది శబ్దాలు హిందీలోనికి వచ్చాయి. వాటిని యథాతదంగాగాని, లేక హిందీభాషా స్వభావాన్ననుసరించి కొద్దిపాటి మార్పుచేసి గాని, हिन्दी లో ప్రయోగించటం జరుగుతుంది.

उदा :

अ) अरबी के शब्द : फेसला, हैजा, कीमत, अल्लाह, ईमान, कायदा, नशा, कसरत, नहर, तरफ, मौसम, वापस, जवाहर, तकिया, दुनिया, अमीर, अदा, अजब, अजीब, अक्ल, असर, अदावत, अजायब, आखिर, आदमी, आदत, इज्जत, इनाम, इस्तीफा, इमारत, इलाज, उम्र, औरत, ओसत, ओलाद, एहसान, कदम, कब्र, कसूर, कसर, कमाल, कर्ज, किस्त, किस्मत, किला, किस्सा, कसम, किताब, कुर्सी, कातिल, खबर, खत्म, खिदमत, खत, खयाल, खराब, गरीब, जलजा, जिस्म, जनाब, जाहिल, जवाब जहाज, जिक्र, जालिम, तकदीर, तमाम, तमाशा, तारीख, तरक्की, तय, तजुर्बा, दवा, दावा, दफ्तर, दावत, दिमाग, दाखिल, दुआ, दगा, दुकान, दौलत, दान, नतीजा, नकल, फकीर, फायदा, बहस, बाकी, मदद, मरजी, मुहावरा, माल, मजबूर, मामूली, मतलब, मालूम, मुकदमा, मुल्लाह, मुक्त, मौका, मुसाफिर, मशहूर, राय, लिहाज, लफ्त, लायक, शराब, वकील, हिम्मत, हरामी, हिसाब, हम, हक, हुक्म, हाल, हाजिर, हमला, हाकिम, हौसला, हजाम, हवालात आदि ।

आ) फारसी शब्द : अफसोस, आतिशबाजी, आबरू, आराम, आवारा, आमदनी, आफत, आईना, आवाज, उम्मीद, कबूतर, कुश्ती, कमरबन्द, किशमिश, किनारा, खाल, खुद, खुश, खरगोश, खामोश, खूब, गुम, गलाह, गरम, गिरफ्तार, गुलाब, गोश्त, चश्मा, चर्खा, चिराग, चादर, चेहरा, चूँकि, चाशनी, जंग, जहर, दिंदगी, जादू, जान, जरमाना, जिगर, जोश, तेज, तनख्वाह, दीवार, देहान्त, दिल, नाव, पलंग, पैदावर, पलक, रेशा, पुल, पारा, पैमाना, बहरा, मजा, मुर्दा, मुफ्त, मुर्गा, मरहम, रंग, राह, लेकिन, लगाम, शादी, शोर, सितार, सरदार, सरकार, सौदागर, हजार, हफ्ता आदि ।

इ) तुर्किशब्द : चम्मच, चुगल, आका, उजबक, उर्दू, कैंची, काबू, कालीन कुली, चिक, चरमक, चेचक, तमगा, तलाश, तीप, बहादूर, बेगम, लफंगा, मुगल, लाश, सुराग, सौगात आदि ।

ई) पुर्तगाली भाषा के शब्द : अनन्नास, आलपीन, अलकता, आलमारी, आया, इस्तरी, इस्पात, कमीज, कमरा, किरानी, काजू, तम्बाकू, फोता, बाल्टी, तौलिया, गोभी, गोदाम, गमला, नीलाम, पादरी, हिस्तौल, बटन, मेज, लबादा आदि ।

उ) अंग्रेजी के शब्द : डांक्टर, इंजीनियर, स्कूल, कॉलेज, प्रोफेसर, बस, स्टेशन, टिकट, स्लेट, अफसर, पुलिस, जज, मिनिस्टर, ऑईर, इंच, एजेंसी, कम्पनी, कमीशन, कमिशनर, क्लास, क्रिकेट, गार्ड, जेल, चेयरमैन, ट्यूशन, डायरी, पेंसिल, पेपर, पेन, नम्बर, नोटिस, नर्स, थर्मामीटर, पार्सल, पेट्रोल, मीटिंग, कोर्ट, कोट, कॉलर, प्रेस, फेम, फोटो, कार, स्कूटर, रिक्शा, साइकिल, मोटर, इंजन, बल्ब, रेडियो, टेलीविजन, कम्यूटर, ट्रेन, क्लर्क कमिटी, वोर्ड, रोड, कैमरा, गेट, टाई, सिनेमा, फिल्म हीरो आदि ।

व्युत्पति: शब्दों का निर्माण वर्णा के मेल से होता है । वर्णों के मिलने से शब्द – खण्ड और शब्द बनाये जाते हैं। शब्द बनाने की यह प्रक्रिया ‘व्युत्पत्ति’ कहलाती है ।

उदाहरण : ‘घर’ शब्द ‘घ’ और ‘र’ दो वर्णों से बना है ।

शब्द – खण्डों के मेल से भी नये शब्द बनते हैं ।

उदा : ‘राज’ और ‘भवन इन दो शब्दों के मेल से ‘राजभवन’ शब्द बना है । वास्तव में ये शब्द खण्ड स्वतंत्र शब्द भी हैं !

संधि था समास की प्रक्रिया के द्वारा शब्द खण्ड (या. स्वतंत्र शब्द ) आपस में मिलकर थोडा बहुत परिवर्तित भी हो जाते हैं। तथा अलग अर्थ देते है ।

उदा ‘सूर्य’ और ‘उदय’ – इन दो शब्दों के मेल से ‘सुर्योदय’ शब्द बना है ।

व्युत्पति की दृष्टि से हिन्दी में शब्दो के तीन प्रकार होते हैं – रूढ़, यौगिक और योगरूढ़ ।

‘रूढ़’ शब्द से आशय वैसे शब्दों से है, जो निरर्थक वर्णों के मेल से बने हैं। जैसे- ‘ठं + डा ठंडा,’ ‘ग + र + म = गरम,’ ‘मी + ठा = मीठा’, ‘ती + ता = तीता’, ‘का + म = काम’, अलग – अलग ये सभी वर्ण निरर्थक हैं, लेकिन ये वर्ण मिलकर अर्थ देंने लगते हैं । ऐसा क्यों है ? ऐसा रूढि [ जन्म से अथवा प्रथा या रिवाज] के चलते हैं । ‘यौगिक’ शब्द वे हैं जो शब्द खण्डों अथवा शब्दों के जुड़ने से बने है । अर्थात इनके खण्ड सार्थक होते हैं ।

उदा : शिव + आलय = शिवालय, विद्य + आलय = विद्यालय, महा + सागर, महासागर, जय + माला = जयमाला, जन + जागरण = जनजागरण, महा + उत्सव महोत्सव आदी ! यहाँ हम देखते हैं कि सभी शब्दांश शार्थक हैं।

‘थोगरूढ़’ उन शब्दों को कहते हैं, जिनके शब्द – खण्ड सार्थक तो होते हैं, लेकिन उनके योग. होने पर शब्द – खण्ड अपने सावान्य अर्थ खोकर एक विशेष अर्थ देते हैं । यह विशेष अर्थ परम्परा से चला आया है ।

उदा : गण (समुह ) + ईश (स्वामी) – गणेश (शिव के पुत्र)

हिम (बर्फ) + आलय (घर) – हिमालय उत्तर में स्थित.

विशाल पर्वत श्रृंखला

जल (पानी) + ज ( जन्मा) – जलज – कमल

चक्र ( पहिया ) + प्राणि (हाथ) – चक्रपाणि (विष्णु)

पीत (पीला) + अम्बर (वस्त्र) + धारी ( धारण करने वाला) – पीतांबरधारी (विष्णु)

धन (बादल) + श्याम (काला) = धनश्याम (कृष्ण)

रचना के आधार पर शब्दों के दो भेद होते है. ।

- विकारी

- अविकारी

विकारी : विकारी शब्द वे हैं, जिनके रूपों में लिंग, वचन तथा. कारक के अनुसार विकार या परिवर्तन आ जाता है ।

लड़का – लड़का, लड़की, लड़के, लड़कों ।

देखना – देख, देखना, देखो, देखी, देखेँ, देखिए ।

वह – वे वहा, तू, तुम, आप

विकारी शब्द है :

- संज्ञा,

- सर्वनाम,

- विशेषण,

- क्रिया

अविकारी : अविकारी वे शब्द हैं जिनके रूप नही बदलते । इनका रूप सभी लिंग, विभक्तियों तथा वचनों में हमेशा एक सा रहता है । परिर्तिन नही होता हे । इसलिए इन्हे अव्यय भी कहते है ।

1. क्रिया विशेषण

2. सम्बन्ध – बोधक

3. समुच्चय बोधक

4. विस्मयादि बोधक

शब्द रचना

हम भाषा का व्यवहार अपने भावों व विचारों के संप्रेषण हेतु करते हैं. ओर कम परिश्रम करके अधिक अर्थ लाना चाहते हैं । अतः शब्दों के आरंभ में अथवा अंत में नये शब्दांश जोड़कर अथवा स्वर या व्यंजनों का परिवर्तन करके हम नया अर्थ लाते है। शब्दों के अरंभ में जुड़नेवाले शब्दांशों को ‘उपसर्ग’ तथा अंत में जुड़नेवाले शब्दांशों को ‘प्रत्यय’ कहा जाता है । अतः इन शब्दांशों से परिचित होना ही इस पाठ का लक्ष्य है ।

उपसर्ग

उपसर्ग में ‘उप’ का अर्थ है- ‘समीप’ तथा ‘सर्ग’ का अर्थ ‘सृष्टि करना’ है । अर्थात ‘उपसर्ग’ उस शब्दांश को कहते हैं, जो शब्द के समीप आकर नया शब्द बनाये । इनके जुड़ने के कारण मूल शब्द के अर्थ में या तो विशेषगुण का प्रतिपादन होता है । अथवा अर्थ बदल जाता है । वस्तुतः अव्यय होने के कारण थे अविकारी होते हैं । अर्थात इनमें लिंग, वचन, कारक आदि के कारण कोई परिवर्तन नही आयेगा । उपसर्गों का स्वतंत्र रूप में उपयोग नही होता । उपसर्गों का विवरण इस प्रकार है –

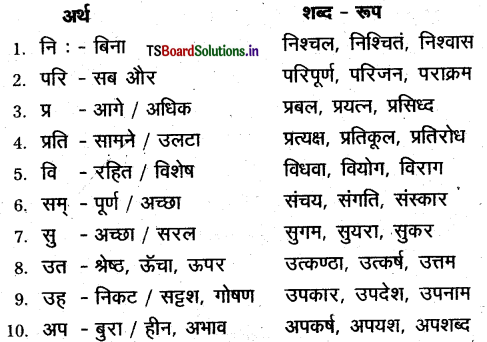

क) संस्कृत के उपसर्ग :

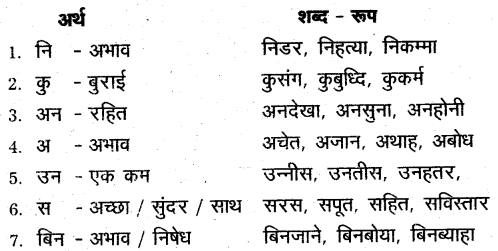

ख) हिन्दी के उपसर्ग :

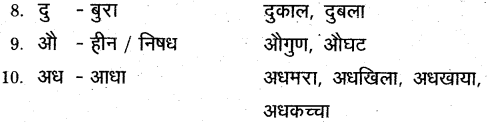

ग) अरबी – फारसी और उर्दू के उपसर्ग :

प्रत्यय

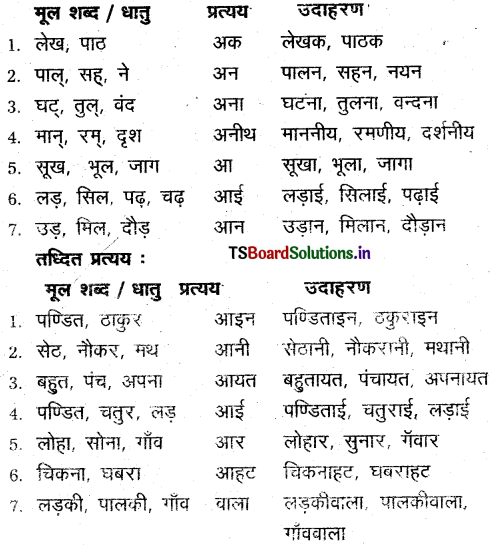

शब्द के पीछे जुडनेवाले शब्दांश को ‘प्रत्यय’ कहा जाता है । प्रत्यय भी उपसर्ग की भांति अव्यय होते हैं । प्रत्यय शब्द में ‘प्रति’ का अर्थ है ‘साथ में’ । फिर अय का अर्थ बनता है. ‘चलनेवाला’ इस प्रकार प्रत्यय का अर्थ वह शब्दांश है जो बाद में जुडता हो । प्रत्यय के दो प्रकार हैं – कृदन्त और तध्दित । जो प्रत्यय क्रिया था धातु के अंत में प्रयुक्त होते हैं, उनको कृत प्रत्यय कहा जाता है । कृत प्रत्यय से बने शब्दों को कृदन्त कहा जाता है । जो धातु को छोड़कर अन्य शब्दों अर्थात् संज्ञा, सर्वनाम व विशेषण से जुड़ते हैं उनको तध्दित प्रत्यय कहा जाता है ।

कृदन्त प्रत्यय :

पर्यायवाची या समानार्थी शब्द

एक ही अर्थ को प्रकट करनेवाले भिन्न- भिन्न शब्दों को पर्यायवाची था समानार्थी शब्द कहा जाता है। जो जितने पर्यायवाची जानता है, वह अपने भावों व विचारों का संप्रेषण उतना ही सफलतापूर्वक कर सकता है । संमानार्थी शब्दों के जानने से शब्द भण्डार में वृध्दि होती है और शब्द भण्डार सफल अभिव्यक्ति का साधन होता है ।

शब्द – पर्यायवाची शब्द

1. आग – अग्नि, अनल, पावक, हुताशन, जातवेद, वैश्वानर

2. घोड़ा – अश्व, हय, वाजि, घोटक, तुरंग, तुरंगम

3. आकाश – नभ, अंबर, आसमान, गगन, व्योम, अंतरिक्ष

4. इच्छा – चाह, अभिलाषा, कामना, वांछा, आकांक्षा, मनोरथ

5. कमल – पंकज, नीरज, राजीव, सरोज, पदम, अरविंद

6. घर – भवन, सदन, मकान, गृह, आवास, निलय

7. नदी – सरिता, तटिनी, तरंगीणी, निर्झरिणी, सलिला

8. पक्षी – खग, विहंग, पखेरू, विहग, परिंदा, अंडज

9. पृथ्वी – भूमि, धरा, धरती, धरणी, वसुधा, धरित्री

10. समुद्र – सागर, जलधि, स्नाकर, पयोधि, जलनिधि, सिंधु

11. सूर्य – दिनकर, भास्कर, रवि, प्रभाकर, आदित्य, मित्र

12. अपमान – अनादर, बेइज्जती, अवमानना, निरादर, तिरस्कार

13. अनुपम – अनुप, अपूर्व, अतुल, अनोखा, अदभूत, अनन्य

14. अनुपम – तम, तिमिर, अंधेरा, अंधियारा, तमस, तमिस

15. जल – पानी, नीर, सलील, वारि, अंबु

16. वायु – पवन, समीर, हवा, मारुत, अनील

17. पेड़ – वृक्ष, तरु, झाड़, विटप

18. नारी – औरत, महिला, स्त्री, सबला

19. मनुष्य – मानव, नर, इंसान, आदमी

20. चाँद – चंद्र, राशि, रजनीश, सोम, कलानिधि

21. दिन – दिवस, दिवा, वार, याम

22. शिक्षक – गुरु; अध्यापक, आचार्य

23. धन – दौलत, संपति, संपदा, किन्त, अर्थ

24. फूल – पुष्प, सुमन, कुसुम

25. माता – माँ, जननी, अम्मा, अंबा

26. अहंकार – दंभ, गर्व, अभिमान, दर्प, मद, घमण्ड

27. अमृत – सुधा, अमिय, पीयुष

28. असुर – दैत्य, दानव, राक्षस, निशाचर

29. अतिथि – अभ्यागत, मेहमान, पाहूना

30. आँख – लोचन, नयन, नेत्र, चक्षु, दूग, विलोचन, अक्षि

31. ईश्वर – प्रभु, परमात्मा, ईश, जगदीश, भगवान, परमेश्वर

32. ओंठ – ओष्ठ, होंठ, अधर

33. क्रोध – रोष, गुस्सा, अमर्ष, नाराज़गी

34. किरण – रश्मी, मरीचि, मयूख, अंशु

35. अलि – भ्रमर, भँवरा, भोरा, षट्पद्, मधुकर, मिलिंद

36. उद्योग – परिश्रम, श्रम, मेहनत, प्रयास, उद्यम

37. पर्वत – पहाड़, गिरि, नग, शैल

38. राजा – नृप, नृपति, सम्राट, नरेश

विलोम शब्द

किसी शब्द के उल्टे या विपरीत अर्थ देनेवाले शब्द को उसका विलोम शब्द कहा जाता है । इन्हें भिन्नार्थक शब्द भी कहा जाता है। इन शब्दों का निर्माण अ, अन, दू, नि आदि उपसर्ग (या) हीन, पूर्ण आदि प्रत्ययों से अथवा कभी – कभी स्वतंत्र शब्द के रूप में भी होता है।

अंत × आदि

अति × अल्प

अपना × पराया

अपराजित × पराजित

अर्वाचीन × प्राचीन

अकाल × सुकाल

अनन्त × अन्त, सान्त

अज्ञ × विज्ञ

अपराधी × निरपराधी

अमृत × विष

अतिथि × आतिथेय

गर्मी × सर्दी

अंकाश × पाताल

घृणा × प्रेम

आचार × अनाचार

जल × थल

इच्छा × अनिच्छा

दया × क्रूरता

इत्थान × पतन

दक्षिण × उत्तर

उपस्थित × अनुपस्थित

दिन × रात

उत्कृष्ट × निकृष्ट

दुर्गन्ध × सुगन्ध

उपकार × अपकार

दुरुपयोग × सजुपयोग

उदघाटन × समापन

दुर × पास

उत्पति × विनाश

धूप × छाँव

उपचार × अपचार

नया × पुराना

उषा × संध्या

नरवर × शाश्वत

उत्तीर्ण × अनुत्तीर्ण

निर्बल × सबल

उल्लास × विषाद

निन्दा × स्तुति

उधार × नकद

निरक्षर × साक्षर

एक × अनेक

प्रश्न × उत्तर

कायर × वीर

बलवान × कमजोर

कडुवा × मीठा

कठिन × सरल

कमजोर × बलवान

शुभ × अशुभ

क्रोध × शान्त

जन्म × मृत्यु

कीर्ति × अपकीर्ति

ज्ञान × अज्ञान

ग्राम × नगर

स्वदेश × विदेश

हिंसा × अहिंसा

लाथक × नालायक

न्याय × अन्याय

कठिनाई × सरलता

उपस्थित × अनुपस्थित

राजा × रंक

आशा × निराशा

गुण × अनगुण / दोष

गलत × सही

स्वीकृत × तिरस्कृत

स्वर्ग × नरक

कृत्रिम × स्वाभाविक

कनिष्ठ × ज्येष्ठ, वरिष्ठ

घीटा × फ़ायदा

जड़ × चेतन

चतुर × मूर्ख

प्रसन्न × अप्रसन्न

भूरि × अल्प